Monoline Lenders

IRD PENALTY CALCULATIONS

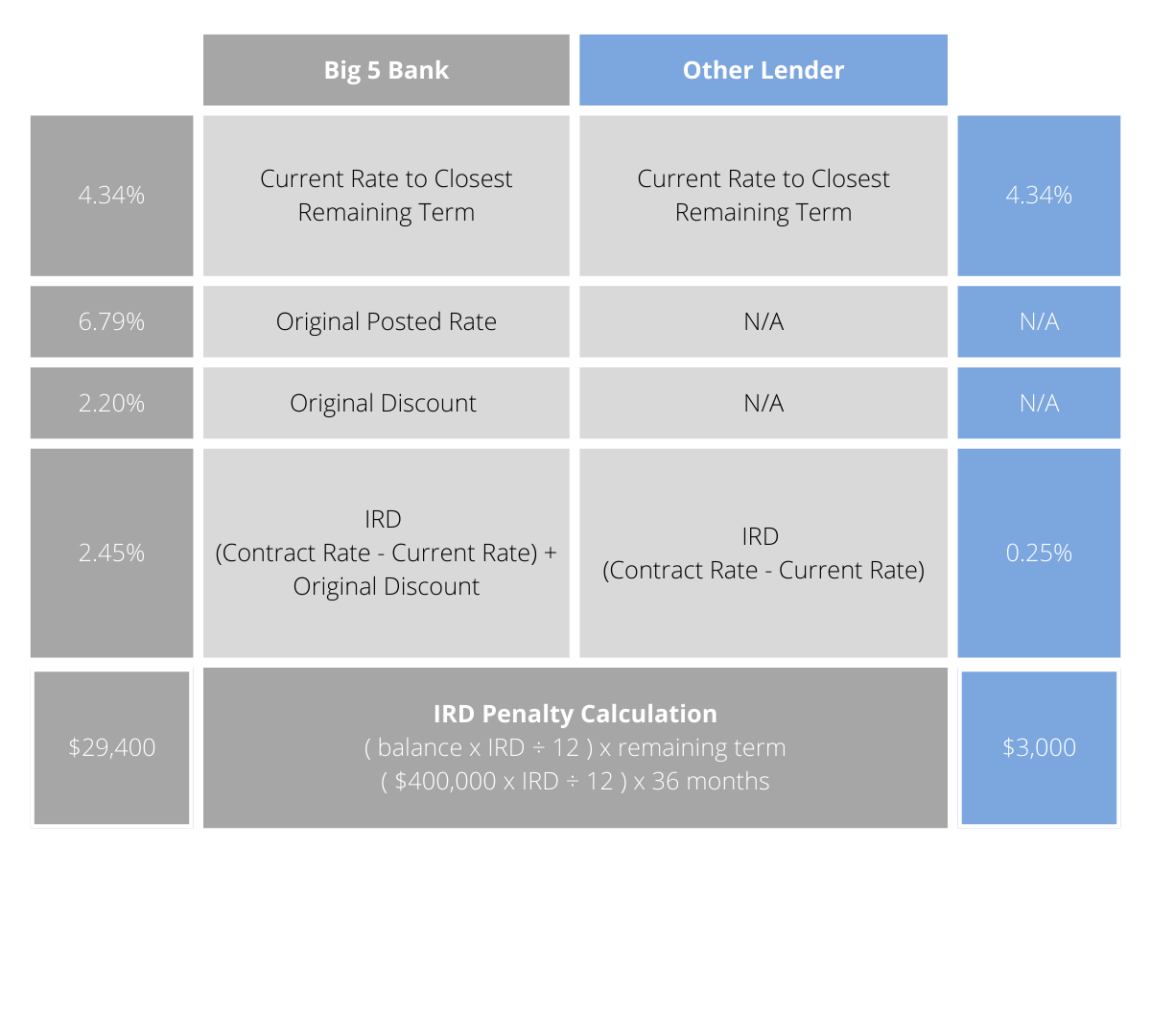

Lenders like the Big 5 Banks offer discounts on their posted rates, unlike monoline lenders, which use lower contract rates upfront. “Discounts” can come back to haunt you, as they are used in the IRD penalty calculation, and the difference can cost clients thousands in interest. Find more information on our Mortgage Penalties info sheet.

In this example, the original

contract rate is 4.59%. At the time of breaking the mortgage, the current balance is

$400,000 with

3 years remaining. With a monoline lender, this would result in

$26,400 in savings compared to a Big Bank.